Some of the offers mentioned below may be expired or not available

‘How do you afford to take all of these trips?’

The first question I’m always asked when people learn of my travels is ‘How do you afford to take all of these trips?” The reality is I use miles and points to cover the largest portion of trips – air travel and hotel stays. Typically my out of pocket costs are just for activities and food. And food costs usually aren’t that high because I am able to leverage my hotel statuses for free breakfasts and lounge access for appetizers, drinks, and snacks.

The quickest and easiest way to earn points and miles is through credit card sign up bonuses and welcome offers. For instance, when the Chase Sapphire Reserve card debuted in 2016, it offered a 100,000 bonus points after spending $4,000 within the first three months of account opening. American Express Platinum card also frequently has 100,000 point welcome offer/bonus.

With just one of these 100,000 point sign up bonuses – you can easily take a week long trip to just about anywhere in the world while having your airfare and hotel stay covered.

And don’t worry about the minimum spend requirement. This course will show you how to meet this amounts even if your typical household budget is not that high.

‘But doesn’t that hurt your credit score?’

The second question I’m always asked is ‘Doesn’t that hurt your credit score?’ The simple answer is not only does it not hurt your credit score, but over the long run it will actually improve your credit score. And I’m going to prove it to you.

Credit Score

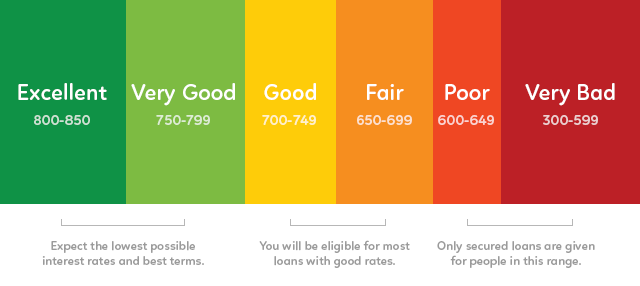

It’s important to understand how your credit score is determined. Most people have no idea how their credit scores are calculated. Different companies, most notably FICO, look at a range of information provided by one of the three major credit reporting agencies – Equifax, Experian, or Transunion – and use that information to create a score that help lenders (mortgage, credit cards, auto loans, etc) predict how likely someone is to pay back the loan on time and how much the loan or credit line should be.

FICO stands for the Fair Isaac Corporation which is the largest and best known companies that calculates a person’s credit score. Though FICO scores are the most widely used among lenders, there are other scores lenders can choose from such as the VantageScore which is becoming more widely used.

There are actually numerous different credit scores, but they generally range from 300-850. The higher the number the better which represents less risk to the lender. Generally a very good or excellent credit score is considered 750 and higher which should get you the best rates when you borrow money.

Factors in a Credit Score

While the exact formula to calculate your credit score is private to each company and unknown to the public, we do know that there are five main factors that go into a credit score. Each has a different effect on your score. Here is the breakdown:

- 35% Payment History – do you have any late payments or do you always pay your bills on time?

- 30% Debt/Amounts Owed – sometimes called ‘credit utilization’. This is basically the ratio of how much you owe divided by your available credit.

- 15% Age of Credit History – the average age of your credit accounts. If you have currently have two credit cards and one of them was opened eight years ago and the second one was opened two years ago – then your average age is five years (8 years + 2 years / 2 credit cards)

- 10% New Credit/Inquiries – how many recent credit inquiries do you have? Companies typically count the number of inquiries in the past two years.

- 10% Mix of Accounts/Types of Credit – typically higher credit scores have a mix of different account types – mortgages, credit cards, auto loans, etc.

You would think that your employment and salary would be important factors in your credit score and your ability to repay loans, but they actually have NO factor in your credit score.

Now that we know all about credit scores, let’s get back to the question ‘Doesn’t that hurt your credit score?’. It’s common to see a very small drop in your credit score immediately after applying for a credit card, but your score will quickly recover and usually surpasses your original score. I’ll show you an example below.

Let me show you why – back to our example above. We currently have two credit cards:

- Credit card #1 – opened 8 years ago with a credit limit of $8,000. We typically use $500/month on this card and pay it off every month.

- Credit card #2 – opened 2 years ago with a credit limit of $10,000. We typically use $1000/month on this card and pay it off every month also.

Let’s assume we were to open credit card #3 today and got approved with another $10,000 credit limit. Let’s see how the credit score factors are effected by opening this new credit card:

- 35% Payment History – no effect since no payments were made yet

- 30% Debt/Amounts Owed – our ‘credit utilization’ is actually decreasing which is good. Instead of spending $1500 per month with an $18,000 credit limit which is 8.3%, our credit utilization is decreasing to 5.3% (still spending $1500 per month but now our credit limit is $28,000)

- 15% Age of Credit History – the new credit card hurts our average age of credit. Instead of a five year average (8 years + 2 years / 2 credit cards); we now have a 3.3 year average (8 years + 2 years + 0 years / 3 credit cards)

- 10% New Credit/Inquiries – this new credit card inquiry will show up on as new credit since and hurt our score a little – this is why you have a small drop in score immediately after applying for the new credit card.

- 10% Mix of Accounts/Types of Credit – no effect since we are opening another credit card – same type of account we currently have

The two items where the new credit card is hurting our credit score account for 25% of our score, but the new credit card also improves our credit utilization which accounts for 30% of our score.

That sounds right, but prove it

While all the above sounds good, I’ve always been a type of person who wants to see proof. So the below information is my personal credit score when I first got into travel hacking:

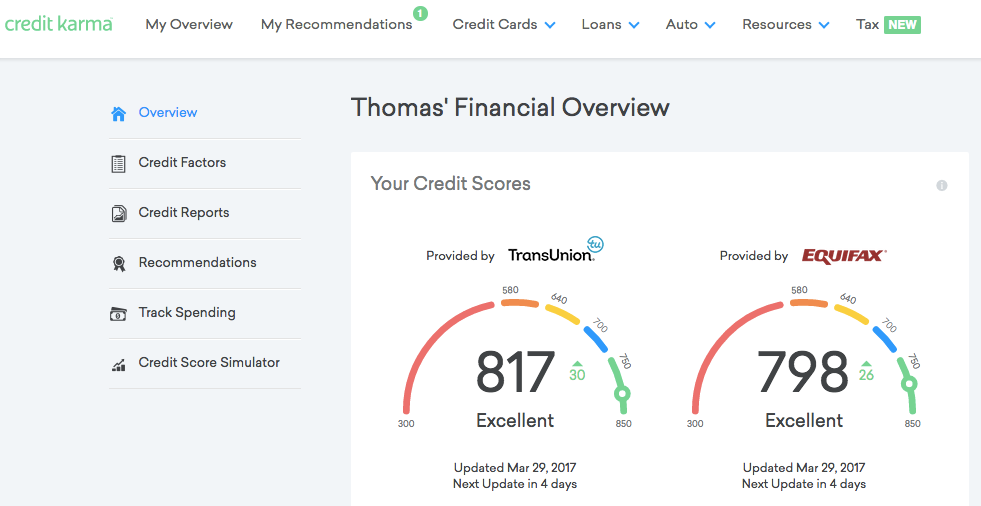

Between March 2015 and March 2017, I have opened 18 credit cards and closed 9 of them. Heck, I even refinanced my mortgage during that period too. Here is my credit score in that 2 year period according to Transunion along with a Google document list of when credit cards were opened and closed:

Transunion

![]()

![]()

Do you remember above when I mentioned your score may drop a slightly when you apply for a new credit card but recovers quickly? Take a look at the chart above.

In January 2017, my credit score was 799. I applied for the Chase Fairmont credit card and was approved. My score dropped a little in February to 787, but then shot back up all the way up to 817.

Hopefully showing you my actual credit scores have set your mind at ease that your credit score won’t be wrecked by applying for multiple credits to earn hundreds of thousands of miles and points.

Check Your Own Credit Score

The government requires the credit bureaus to provide you a free credit report once every 12 months from AnnualCreditReport.com. If you have never requested a copy, feel free to request it now – either from one of three credit bureaus or all three. It’s not the easiest process and the information is not presented in the most easy to understand format.

Did you end up getting a copy? It’s not really user friendly, right? The services listed below also provide you a free credit score updated throughout the year either daily, weekly, or monthly. Most offer additional data taken directly from your credit reports that is easy to understand.

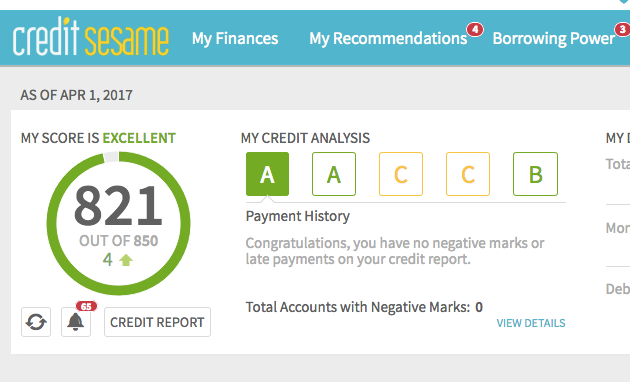

Credit Sesame – provides you with a credit score each month based upon Transunion. Credit Sesame also provides free daily credit monitoring with alerts by email, text or their app. They also provide identity theft insurance and help to restore your identity in case of theft.

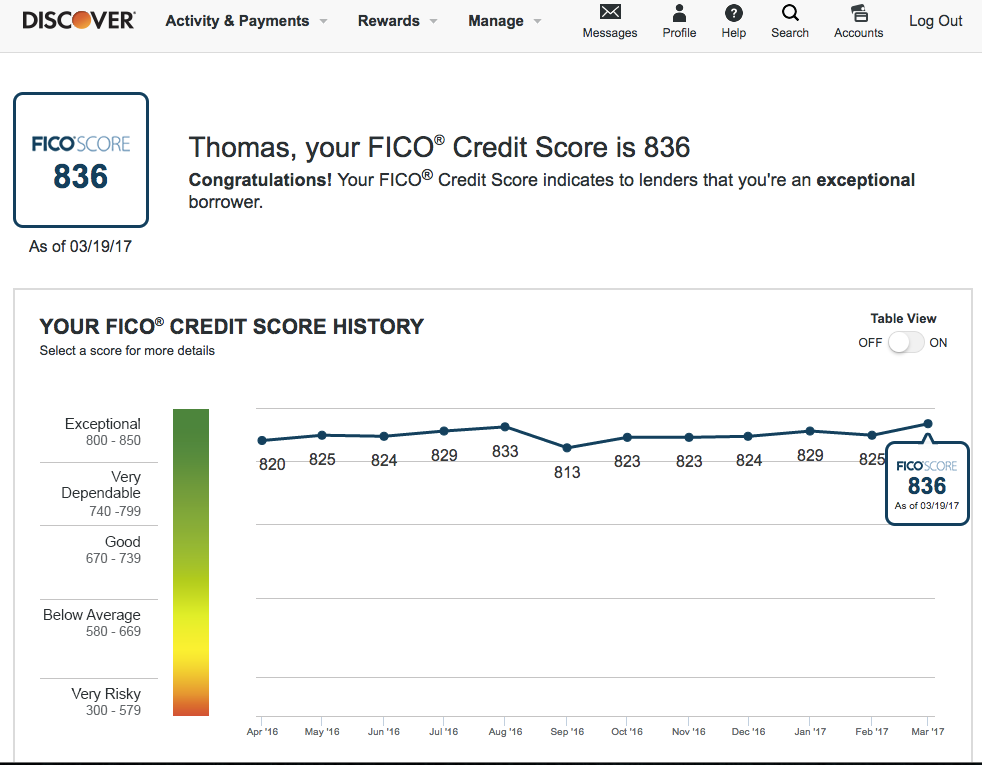

Discover – Discover offer a free FICO credit score even if you aren’t a customer. They graph your score over the past year. Other credit card companies provide free credit scores to certain card holders – if you already have a credit card – check to see if your issuer provides one.

CreditKarma – this is the site I use the most. It offers you both Transunion and Equifax scores on one screen. It also has a user friendly interface. It also lists all of the accounts that you have opened and closed.

Need to Knows

- There are many factors (payment history, age & type of credit, etc) that affect a person’t credit score

- Opening new credit cards may lower your credit score by a few points in the very short term, but will ultimately increase your credit score

- The quickest and easiest way to earn large amounts of miles and points to use for almost free travel is through credit card sign-up bonuses

Homework

- Sign up at one of the three sites listed above to track your own credit score throughout this journey.

So did I convince you that signing up for multiple credit cards to obtain hundreds of thousands miles and points won’t ruin your credit?